Sukuk al-Murabaha

Although the sukuk al-murabaha structure is less commonly used in comparison to some of the other sukuk structures described in this Chapter 2 (Sukuk Structures), it could be considered as a possible alternative where it is not possible to identify a tangible asset for the purposes of the underlying investment.

In the Islamic finance industry, the term murabaha is broadly understood to refer to a contractual arrangement between a financier (the seller) and a customer (the purchaser) whereby the financier would sell specified assets or commodities to the customer for spot delivery in the expectation that the customer would be able to meet its deferred payment obligations under the murabaha agreement.

The deferred price would typically include the cost price at which the financier had purchased the assets/commodities, plus a pre-agreed mark- up representing the profit generated from its involvement in the transaction. The payments of the deferred price from the customer may be structured as periodical payments on dates specified at the outset, thus creating an income stream for the financier for the term of the transaction.

The same characteristics of the murabaha structure can also be adapted for use as the underlying structure in a sukuk issuance. Sukuk proceeds from Investors may be applied by Issuer SPV to acquire commodities and on- sell such commodities to the Originator to generate revenue from the murabaha deferred price which would be distributed to the Investors throughout the term of the sukuk al- murabaha.

As the sukuk certificates in a sukuk al-murabaha essentially represent entitlements to shares in receivables from the purchaser of the underlying murababa, they are not negotiable instruments that can be traded on the secondary market because Shari’a does not permit trading in debt except at par value. This reduces the popularity of sukuk al-murabaha for potential investors and is reflected by the limited number of sukuk al-murabaha issuances in the sukuk market. An example of a sukuk al-murabaha issuance is: Arcapita Bank, US$200million issued in October 2005.

Despite being debt instruments, sukuk al- murabaha certificates may still be negotiable if they form a small part of a larger portfolio comprising mostly of other negotiable instruments such as sukuk al-ijara, sukuk al- musharaka, and/or sukuk al-mudaraba.

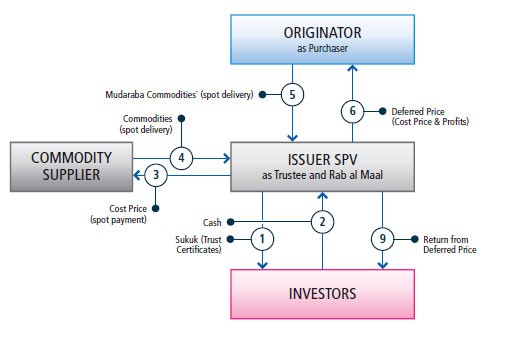

Set out on the following page is an example of a typical sukuk al-murabaha structure

Figure 1: Structure of Sukuk al-Murabaha

Overview of Structure

- Issuer SPV issues sukuk, which represent an undivided ownership interest in an underlying asset or transaction. They also represent a right against Issuer SPV to payment of the Deferred Price.

- The Investors subscribe for sukuk and pay the proceeds to Issuer SPV (the “Principal Amount”). Issuer SPV declares a trust over the proceeds (and any commodities acquired using the proceeds – see paragraph 3 below) and thereby acts as Trustee on behalf of the Investors.

- Originator (as Purchaser) enters into a murabaha agreement with Trustee (as Seller), pursuant to which Trustee agrees to sell, and Originator agrees to purchase, certain commodities (the “Commodities”) from Trustee on spot delivery and deferred payment terms. The period for the payment of the deferred price will reflect the maturity of the sukuk. Trustee purchases the Commodities from a third party Commodity Supplier for a Cost Price representing the Principal Amount for spot payment.

- Commodity Supplier makes spot delivery of the Commodities to Trustee in consideration for the Cost Price.

- Trustee (as Seller) on-sells to Originator the Commodities upon delivery from Commodity Supplier in accordance with the terms of the murabaha agreement

- Originator (as Purchaser) makes payments of deferred price at regular intervals to Trustee (as Seller). The amount of each deferred price instalment is equal to the returns payable under the sukuk at that time.

- Issuer SPV pays each deferred price instalment to the Investors using the proceeds it has received from Originator.

Key Features of the Underlying Structure

Set out below is a summary of the basic requirements which should be considered when using murabaha as the underlying structure for the issuance of sukuk:

- The consideration (deferred price) must be at an agreed rate and for an agreed period;

- In order to ensure that Issuer SPV obtains marketable title to the Commodities from Commodity Supplier to facilitate their on- sale to Originator, Issuer SPV may require certain representations and warranties from the Commodity Suppler that the Commodities will be purchased free of any encumbrances or liens;

- During the period of ownership of the Commodities by Issuer SPV, there is a risk of price fluctuation in the market value of the Commodities which can be mitigated by minimising the duration of Issuer SPV’s ownership and specifying the deferred price payable by Originator (as Purchaser;

- If Originator requests physical delivery (as opposed to constructive delivery), there may be a risk that the Commodities are damaged whilst in transit which may be mitigated by undertakings from Originator in the murabaha agreement to accept the Commodities on an “as is” basis;

- To streamline the administrative processes involved in the purchase of the Commodities from the Commodity Supplier and its immediate on-sale to the Purchaser, the Trustee may appoint the Originator as its buying agent under a buying agency agreement to buy the commodities from the Commodity Supplier in its capacity as agent. Following the purchase of Commodities from the Commodity Supplier, the Trustee would (as principal) sell the same Commodities to the Originator (as Purchaser); and

- Depending on the type of Commodities involved, and the jurisdiction of the parties, tax liabilities in respect of the acquisition and sale of the Commodities should be considered in order to maximise the preservation of the Principal Amount in the Cost Price

Required Documentation

The following documentation is typically required for a sukuk al-istithmar transaction:

| Document | Parties | Summary / Purpose |

|---|---|---|

| Murabaha Agreement | Originator (as Purchaser) and Trustee (as Seller) | Trustee (and the Investor) sells Commodities to Originator on spot delivery and deferred payment terms. Documents the terms of the murabaha sale transaction as well as terms of payment of deferred price. |

| Sale and Purchase Agreement | Trustee (as Buyer) and Commodity Supplier (as Supplier) | Commodity Supplier sells Commodities to Trustee on spot delivery and spot payment terms |

Related Structures/Structural Developments

Shari’a prohibits the trading of debt receivables, particularly when doing so at a discount may give rise to interest (riba). As discussed earlier, this limits the negotiability of sukuk certificates issued under the sukuk al-murabaha structure as such certificates essentially represent entitlements to shares of debt receivables from the purchaser of the underlying murabaha, and this structure has thus been less commonly used in recent times. However, the following should also be noted:

- Sukuk al-murabaha certificates would be negotiable if they were issued prior to the sale of the murabaha commodities from the Originator to the underlying purchaser. This is because the Shari’a analysis turns on whether there is some ongoing ownership stake between the Investor and the sukuk asset following a transfer of the sukuk certificate (which is permitted) or whether the transfer shifts ownership and creates a debt obligation on a third party (not permitted). As such, sukuk certificates issued prior to a murabaha commodity sale would represent ownership in those commodities rather than the right to the receivables generated by their sale;

- The transfer of sukuk al-murabaha certificates is permitted even if they are issued after the sale of commodities under the underlying murabaha, so long as they are traded at face value (rather than sold at a discount or a profit); and

- Sukuk certificates derived from an underlying murabaha structure may still be negotiable if the murabaha receivables form a small proportion (exact percentages may vary depending on the transaction and the analysis of each Shari’a scholar) of a larger portfolio of sukuk assets comprising mostly other negotiable instruments such as sukuk al-ijara, sukuk al-musharaka, and/or sukuk al-mudaraba.

Despite the global downturn in sukuk issuance in 2008, issuances based on the sukuk al-murabaha structure increased by nearly 60%4 . Whilst sukuk al-murabaha issuances still only account for a small fraction of the total value of the sukuk market, the increased number of issuances suggest that the structure is still favoured for smaller deals, where the Investors are more likely to be buy-to-hold investors hence more immune to uncertainties over negotiability

This article was originally published in the Dubai International Financial Centre Sukuk Guidebook. The article is reproduced on this website with the kind permission of the Dubai International Financial Centre (DIFC).