Sukuk al-Istisna

Alternatively referred to as the “Islamic project bond”, the structure of sukuk al-istisna has not been that widely used. Although, at first glance, the structure appears ideal for the financing of greenfield development, certain structural drawbacks have proven difficult to overcome and, as a result, sukuk al-istisna has not featured as an alternative source of Islamic funding on multi-sourced project financing in the manner once predicted.

Of particular significance is the prevailing view that sukuk al-istisna are not tradable during the construction period. In addition to this, the different approaches taken by Shari’a scholars to advance rentals and istisna termination payments have also led structurers to consider other more ‘flexible’ structures (such as sukuk al-musharaka).

Broadly speaking, istisna translates as being ‘to order a manufacturer to manufacture a specific good for the purchaser’. Under an istisna, it is important that the price and specification of the good to be manufactured are agreed at the outset.

In the modern day context of Islamic finance, the istisna has developed into a particularly useful tool in the Islamic funding of the construction phase of a project – it is often regarded as being similar to a fixed-price ‘turnkey’ contract. In order to enable investors to receive a return during the period where assets are being constructed under an istisna arrangement, some Shari’a scholars have permitted the use of a forward lease arrangement (known as ijara mawsufah f al-dimmah) alongside such istisna arrangement.

Accordingly, sukuk al-istisna often combines an istisna arrangement with a forward lease arrangement – whilst the istisna is the method through which the investors can advance funds to an originator, the ijara provides the most compatible payment method to those investors.

The use of staged payments (a common feature in istisna construction arrangements – see further below) may however result in an unutilised amount of sukuk proceeds being held in the structure for a prolonged period during construction (pending the achievement of the relevant milestones).

Accordingly, it may be necessary to consider investing these amounts in Shari’a-compliant investments in order to mitigate negative carry (i.e. periodic distributions continue to be payable whilst cash remains unutilised – a position which is likely to be unacceptable to the originator).

It should, however, be noted that this approach to investment of the unutilised sukuk proceeds has received some criticism.

As of the date of publication, there are no sukuk al-istisna issuances listed by originators on NASDAQ Dubai.

The Qatar Real Estate Investment Company (QREIC) sukuk offering in 2006, which has an istisna component to its structure, is listed on the Euro MTF market of the Luxembourg Stock Exchange. The 2008 issue of a second sukuk by National Central Cooling Company (Tabreed) also has an istisna and is listed on the London Stock Exchange.

Set out in the following page is a basic example of a sukuk al-istisna structure.

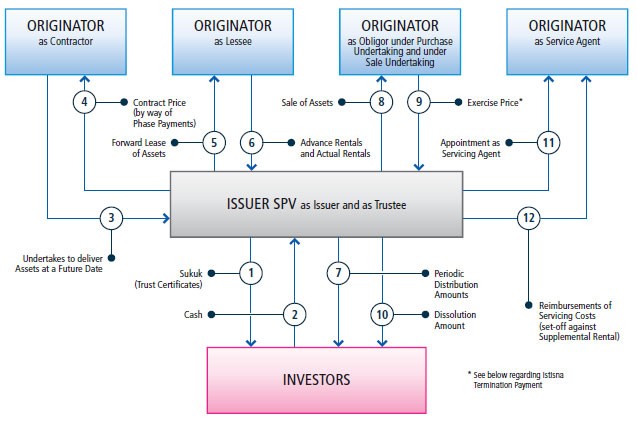

Figure 1: Structure of Sukuk al-Istisna

Overview of Structure

- Issuer SPV issues sukuk, which represent an undivided ownership interest in an underlying asset or transaction. They also represent a right against Issuer SPV to payment of the Periodic Distribution Amount and the Dissolution Amount.

- The Investors subscribe for sukuk and pay the proceeds to Issuer SPV (the “Principal Amount”).

- Issuer SPV declares a trust over the proceeds (and any assets acquired using the proceeds - see paragraph 3 below) and thereby acts as Trustee on behalf of the Investors.

- Originator enters into an istisna arrangement with Trustee, pursuant to which Originator agrees to manufacture or construct certain assets (the “Assets”) and undertakes to deliver those Assets at a future date, and Trustee agrees to commission those Assets for delivery at such future date.

- Trustee pays a price (typically by way of staged payments against certain milestones) to Originator as consideration for the Assets in an aggregate amount equal to the Principal Amount. DIFC Sukuk Guidebook 42 Trustee undertakes to lease the Assets to Originator under a forward lease arrangement (known as ijara mawsufah f al-dimmah) for an overall term that reflects the maturity of the sukuk.

- Originator (as Lessee) makes payments of: Advance Rental prior to the delivery (i). of the Assets; and Actual Rental following the delivery (ii). of the Assets, at regular intervals to Trustee (as Lessor) in amounts which are equal to the Periodic Distribution Amount payable under the sukuk at that time. These amounts may be calculated by reference to a fixed rate or variable rate (e.g. LIBOR or EIBOR) depending on the denomination of sukuk issued and subject to mutual agreement of the parties in advance.

- Issuer SPV pays each Periodic Distribution Amount to the Investors using the Advance Rental or, as the case may be, the Actual Rental it has received from Originator.

- Provided that delivery of the Assets has occurred, upon:

- an event of default or at maturity (at the option of Trustee under the Purchase Undertaking); or

- the exercise of an optional call (if applicable to the sukuk) or the occurrence of a tax event (both at the option of Originator under the Sale Undertaking),

- Payment of Exercise Price by Originator (as Obligor) or, if termination occurs prior to delivery of the Assets, payment of the Istisna Termination Payment by Originator (as Contractor).

- Issuer SPV pays the Dissolution Amount to the Investors using the Exercise Price (or, if termination occurs prior to delivery of the Assets, the Istisna Termination Payment) it has received from Originator.

- Trustee and Originator will enter into a service agency agreement whereby Trustee will appoint Originator as its Servicing Agent, on and from delivery of the Assets, to carry out certain of its obligations under the forward lease arrangement, namely the obligation to undertake any major maintenance, insurance (or takaful) and payment of taxes in connection with the Assets. To the extent that Originator (as Servicing Agent) claims any costs and expenses for performing these obligations (the “Servicing Costs”) the Actual Rental for the subsequent lease period under the forward lease arrangement will be increased by an equivalent amount (a “Supplemental Rental”). This Supplemental Rental due from Originator (as Lessee) will be set off against the obligation of Trustee to pay the Servicing Costs.

Key Features of the Underlying Structure

Set out below is a summary of the basic requirements that should be considered when using a combination of istisna and forward leasing as the underlying structure for the issuance of sukuk:

- The price and specifications for the good or asset need to be specified at the outset;

- It is quite common for the purchaser to split the purchase price (paid in advance) into staged payments that correspond to certain milestones that are agreed upfront with the contractor;

- Although it is not necessary to fix the time of delivery under the istisna, the purchaser may elect to fix a maximum time for delivery - this essentially means that, if the contractor delays delivery after the scheduled completion date, the purchaser will not be bound to accept the goods and to pay the price;

- Liquidated damages provisions may be included in order to incentivise the contractor to deliver on schedule (and to mitigate late delivery risk);

- Although not universally accepted, the majority of Shari’a scholars consider forward leasing permissible on the understanding that: advance rentals are taken into account (as rental which has been paid) and have to be refunded in full if the assets are never actually delivered for leasing.

- Such matters have to be carefully addressed in the documentation in order to ensure that the commercial deal is not disturbed: for example, by careful calculation of any termination payments that are triggered if a termination occurs pre-delivery (i.e. it becomes necessary to ensure that the amount payable by the contractor upon termination of the istisna arrangement is sufficient to cover the Dissolution Amount); and

- Following delivery of the asset(s), the basic requirements of an ijara discussed earlier in this Chapter 2 (Sukuk Structures) at Part 1: Sukuk al-Ijara in the section titled ‘Key Features of the Underlying Structure’ would otherwise apply.

The above requirements are based on the principles set out in AAOIFI Shari’a Standard No. 11 (Istisna and Parallel Istisna) and other established principles relating to istisna.

Required Documentation

The following documentation is typically required for a sukuk al-istithmar transaction:

| Document | Parties | Summary / Purpose |

|---|---|---|

| Istisna AgreementMudaraba Agreement | Originator (as Contractor) and Trustee (as Purchaser) | From Trustee›s (and the Investors›) perspective, this is the document that gives ownership of revenue generating assets (i.e. the Assets) at a future date. From Originator’s perspective, this is the document under which it receives funding. Certain termination rights are granted to Trustee such that, prior to delivery of the Assets, Trustee is able to claim a refund and compensation amount (by way of an Istisna Termination Payment) sufficient to cover the Dissolution Amount. |

| Forward Lease (Ijara Mawsufah f al-Dimmah) Agreement | Trustee (as Lessor) and Originator (as Lessee) | This contains an undertaking to lease such that, following delivery of the Assets, Trustee leases the Assets to Originator in a manner that: gives Originator possession and use of the i. Assets so that its principal business can continue without interruption; and through Actual Rentals it generates a debt- ii. based return for Trustee (and the Investors). Prior to delivery of the Assets, Advance Rentals are paid by Originator in order to generate a debt-based return for Trustee (and the Investors). |

| Service Agency Agreement | Trustee (as Lessor / Principal) and Originator (as Servicing Agent) | On and from delivery of the Assets, this allows Trustee to pass responsibility for major maintenance, insurance (or takaful) and payment of taxes (i.e. an owner’s obligations) back to Originator. Any reimbursement amounts or service charges payable to Servicing Agent are set off against (i) a corresponding ‘supplementary rental’ under the Forward Lease or (ii) an additional amount which is added to the Exercise Price… |

| (payable under the Purchase Undertaking or the Sale Undertaking, as applicable). | ||

| Purchase Undertaking (Wa’d) | Granted by Originator (as Obligor) in favour of Trustee | Allows Trustee to sell the Assets back to Originator if an event of default occurs or at maturity, in return for which Originator is required to pay all outstanding amounts (through an Exercise Price) so that Trustee can pay the Investors. Applies only on and from delivery of the Assets. |

| Sale Undertaking (Wa’d) | Granted by Trustee in favour of Originator (as Obligor) |

Structural Developments/AAOIFI’s Statement of 2008

The following structural refinements are possible in respect of the sukuk al-istisna structure described above:

- If legal and/or registered title to a particular asset exists and (due to, by way of example, the prohibitive cost implications or tax implications of registering such a transfer of title) it is not possible to transfer that legal / registered title, it may be possible, depending on the asset type and the view taken by the relevant Shari’a scholars, to rely upon the concept of beneficial ownership in structuring a sukuk al-istisna transaction. The istisna agreement (in the structure discussed above) would document the transfer to the trustee of the beneficial ownership interest in the underlying asset - and such beneficial ownership interest would be sufficient to enable the trustee’s entry into the forward leasing arrangements contemplated in the example above; and

- Some Shari’a scholars regard the istisna arrangement as one that has to be entered into strictly between the purchaser and the contractor – and that the contractor has to be the person who will actually construct or manufacture the asset. Adopting this approach, the Trustee would be required to have a relationship directly with the ultimate contractor / manufacturer and not the Originator. In order to avoid the difficulties of such an analysis, it is sometimes necessary to re-characterise the istisna arrangement as a procurement arrangement, whereby the Originator is obliged to procure the construction / manufacture and delivery of the underlying asset(s). The Originator thereby retains the direct contractual relationship with the ultimate contractor / manufacturer.

For latest information and data on sukuk, see the IslamicBanker Sukuk Monitor.

For more information, please see our Education resources on: Istisna'.

This article was originally published in the Dubai International Financial Centre Sukuk Guidebook. The article is reproduced on this website with the kind permission of the Dubai International Financial Centre (DIFC).