Sukuk al-Istithmar

The first step in structuring a sukuk is often to analyse what exactly the business of an originator entails and what assets (if any) are available to support the issuance of sukuk. If it is not possible to identify a tangible asset and the business of such originator is largely ‘intangible’, then structuring a sukuk issuance can still be achieved (although not universally accepted).

Perhaps the best examples of this involve Islamic financial institutions and their rights to receivables under a variety of different Islamic financing techniques (evidenced through Islamic contracts with these institutions’ customers / clients). It is possible for the rights under these Islamic contracts to be packaged together and ‘sold’ in order to form the underlying basis for issuing sukuk. However, care needs to be taken so as to ensure that this is not construed as trading in debt.

The term “istithmar” is broadly understood to mean an “investment”. Under a sukuk al-istithmar structure it is possible for ijara contracts (and the relevant underlying assets), murabaha receivables, and/or istisna receivables (each generated by the originator), as well as shares and/or sukuk certificates to be packaged together and sold as an investment. The income generated by such investment can then be used to make payments to the investors under the sukuk.

As of the date of publication, there are no sukuk al-istithmar issuances listed by originators on NASDAQ Dubai.

Examples of sukuk al-istithmar issuances advised on by Clifford Chance LLP and listed elsewhere include Islamic Development Bank’s 2009 issuance (listed on the London Stock Exchange).

Set out in the following page is an example of a sukuk al-istithmar structure, sometimes referred to as investment agency sukuk:

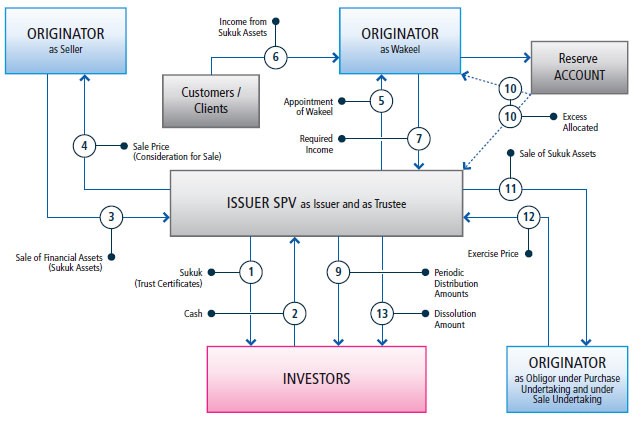

Figure 1: Structure of Sukuk al-Istithmar

Overview of Structure (Using the numbering from Figure 7 above)

- Issuer SPV issues sukuk, which represent an undivided ownership interest in an underlying asset or transaction. They also represent a right against Issuer SPV to payment of the Periodic Distribution Amount and the Dissolution Amount.

- The Investors subscribe for sukuk and pay the proceeds to Issuer SPV (the “Principal Amount”). Issuer SPV declares a trust over the proceeds (and any assets acquired using the proceeds – see paragraph 3 below) and thereby acts as Trustee on behalf of the Investors.

- Originator enters into a sale and purchase arrangement with Trustee, pursuant to which Originator agrees to sell, and Trustee agrees to purchase, a portfolio of certain financial assets (the “Sukuk Assets”) from Originator.

- Trustee pays the purchase price to Originator as consideration for its purchase of the Sukuk Assets in an amount equal to the Principal Amount.

- Trustee appoints Originator as its wakeel (or agent) with respect to the Sukuk Assets for a term that reflects the maturity of the sukuk. Originator is responsible for servicing the Sukuk Assets and, in particular, collection of the income (comprising principal and profit) therefrom.

- Originator collects income in respect of the Sukuk Assets from the relevant customers / clients and will deposit these amounts into a collection account (the “Collection Account”).

- At regular intervals, corresponding to Periodic Distribution Dates, Originator will be required to make income payments to Trustee in respect of the Sukuk Assets. This will be achieved through a target amount (the “Required Income”) which is agreed for each collection period. The amount of Required Income during a collection period will be equal to the Periodic Distribution Amount payable under the sukuk at that time. This amount may be calculated by reference to a fixed rate or variable rate (e.g. LIBOR or EIBOR) depending on the denomination of sukuk issued and subject to mutual agreement of the parties in advance.

- During a particular collection period, if the income amount collected in respect of the Sukuk Assets (as reflected in the Collection Account) is in excess of the Required Income such excess can either be:

- credited to a reserve account (the “Reserve Account”) with Originator; or

- in a case where a financial asset has matured (and principal therefrom has been repaid by the customer / client), and in order to avoid excess cash in the structure, used to purchase additional financial assets under the purchase arrangement referred to in paragraph 3 above (and which will then become Sukuk Assets).

The balance in the Reserve Account (if any) can also be used to cover a shortfall in collections to meet the Required Income in any given collection period. In the event that there is a shortfall in both collections and the Reserve Account, it may be permissible for Originator to make an on-account payment or to provide Shari’a-compliant liquidity funding to bridge any gap in funding.

- Issuer SPV pays each Periodic Distribution Amount to the Investors using the Required Income it has received from Originator.

- Upon redemption of the sukuk (see paragraph 11 below), the balance of the Reserve Account (if any) will be paid (being the “Distributed Reserve Amount”) to Trustee in order to enable the payment of the Dissolution Amount to the Investors. The excess (if any) will be retained by Originator as incentive fees.

- Upon

- an event of default or at maturity (at the option of Trustee under the Purchase Undertaking); or

- the exercise of an optional call (if applicable to the sukuk) or the occurrence of a tax event (both at the option of Originator under the Sale Undertaking),

Trustee will sell, and Originator will purchase, the Sukuk Assets at the applicable Exercise Price, which will be equal to the Principal Amount plus any accrued but unpaid Periodic Distribution Amounts owing to the Investors less the

Distributed Reserve Amount (if any)

- Payment of Exercise Price by Originator (as Obligor).

- Issuer SPV pays the Dissolution Amount to the Investors using the Exercise Price and the Distributed Reserve Amount (if any) it has received from Originator.

Key Features of the Underlying Structure

Set out below is a summary of the basic requirements that should be considered when using sukuk al-istithmar:

- It is likely that the customers / clients to whom the financial assets (comprised in the sukuk assets) relate will need to be informed about (and, in some instances, requested to consent to) the sale of those financial assets to the Trustee and the role of the Originator in acting on the trustee’s behalf;

- In order to ensure the continuing acceptance and tradability of the sukuk, it will be necessary to introduce safeguards into the documentation to ensure that the net asset value of ijara contracts (together with underlying assets), shares and asset- based sukuk certificates (i.e. non-sukuk al- murabaha) comprised in the sukuk assets as at any given date is not less than 30%5 of the net asset value of the sukuk assets (taken as a whole) as at the closing date;

- The role of a custodian may be required in order to ensure that the sukuk assets are sufficiently segregated from the other financial assets of the Originator;

- Principal amounts from the underlying financial assets should never be used to service coupon payments under the sukuk and

- Although the wakala arrangement will require an upfront fee to be paid to the Originator (as wakeel), this can be combined with incentive fees payable a maturity based on the overall performance of the sukuk assets (but care should be taken to ensure that this does not amount to profit-sharing).

The above requirements are based on the principles set out in AAOIFI Shari’a Standards No. 17 (Investment Sukuk), No. 21 Financial Paper (Shares and Bonds) and No. 23 (Agency) and other established principles relating to the concept of istithmar

Required Documentation

The following documentation is typically required for a sukuk al-istithmar transaction:

| Document | Parties | Summary / Purpose |

|---|---|---|

| Sale and Purchase Agreement | Originator (as Seller) and Trustee (as Purchaser) | From Trustee’s (and the Investors›) perspective, this is the document that gives ownership of revenue- generating financial assets (i.e. the Sukuk Assets). From Originator’s perspective, this is the document under which it receives funding. |

| Wakala Agreement | Trustee (as Principal) and Originator (as Wakeel) | Trustee appoints Originator as Wakeel (or agent) in respect of the servicing of the Sukuk Assets, such that: Originator retains control of the Sukuk Assets so that its principal business can continue without interruption; and through collection of income and the target level of Required Income, it generates a return for Trustee (and the Investors). |

| Purchase Undertaking (Wa’d) | Granted by Originator (as Obligor) in favour of Trustee | Allows Trustee to sell the Sukuk Assets back to Originator if an event of default occurs or at maturity in return for which Originator is required to pay all outstanding amounts (through an Exercise Price) so that Trustee can pay the Investors. |

| Sale Undertaking (Wa’d) | Granted by Trustee in favour of Originator (as Obligor) | Allows Originator to buy the Sukuk Assets back from Trustee in limited circumstances (e.g., the occurrence of a tax event), in return for which Originator is required to pay all outstanding amounts (through an Exercise Price) so that Trustee can pay the Investors. |

Structural Developments and Observations

Despite similarities in certain structural features, sukuk al-istithmar should be distinguished from sukuk al-mudaraba and sukuk al-wakala.

The following aspects of a sukuk al-istithmar issuance warrant further consideration:

- There are differing views as to how a shortfall during a collection period should be remedied – some Shari’a scholars would prefer to avoid using the purchase undertaking in this scenario and would instead look to the Originator to make good any shortfall through either on-account payments or provision of Shari’a-compliant liquidity funding. These arrangements are however not without their own difficulties;

- There are also differing opinions between the Shari’a scholars as to what is required (in terms of minimum thresholds and asset types) in order to maintain the tradability of the sukuk; and

- It may be necessary for certain roles of the Originator to be performed by another entity altogether and/or for a sub-agency or delegation arrangement to be put in place in order to overcome any residual concerns over the entity that will ultimately provide the purchase undertaking.

For latest information and data on sukuk, see the IslamicBanker Sukuk Monitor.

This article was originally published in the Dubai International Financial Centre Sukuk Guidebook. The article is reproduced on this website with the kind permission of the Dubai International Financial Centre (DIFC).